Depreciation schedules and disposal timing are more closely connected than many organisations realise. The point at which IT equipment is fully depreciated on your books does not necessarily align with the optimal time to dispose of it from a financial, operational, or security perspective. Understanding this relationship helps you make smarter decisions about when to retire equipment.

How IT Depreciation Works in Australia

In Australia, IT equipment is typically depreciated over its effective life as determined by the Australian Taxation Office. The ATO’s effective life guidelines suggest different periods for different equipment categories. Computers and laptops are generally depreciated over four years. Servers may be depreciated over four to five years. Networking equipment varies from three to five years depending on type. Mobile devices are typically three years.

Organisations can use either the prime cost (straight-line) or diminishing value method. Under the prime cost method, a $2,000 laptop depreciates by $500 per year over four years. Under the diminishing value method, depreciation is higher in earlier years and lower in later years, which more closely reflects the actual pattern of value decline in IT equipment.

The Depreciation-Disposal Disconnect

A common approach is to dispose of equipment when it reaches the end of its depreciation schedule, on the assumption that zero book value means the asset has no remaining useful life. But this creates a disconnect in several ways.

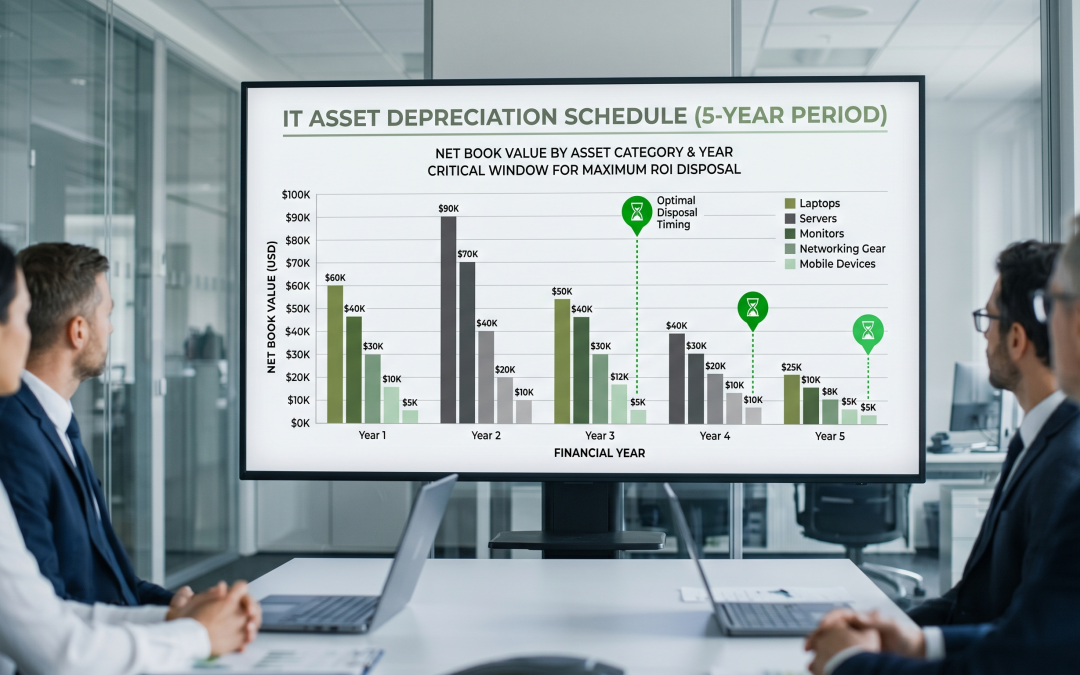

Equipment may still be perfectly functional and valuable on the secondary market when it reaches zero book value. A laptop that is fully depreciated at four years may still be worth $200-400 on the resale market. Disposing of it promptly at the end of its depreciation schedule captures this value. Waiting longer reduces the recovery.

Conversely, some equipment becomes operationally obsolete before it is fully depreciated. A server that can no longer meet performance requirements at two years should be replaced regardless of its remaining book value. In this case, the remaining depreciation is written off at disposal.

Financial Implications of Disposal Timing

The timing of disposal creates several financial effects. If equipment is disposed before full depreciation, the remaining book value can be written off as a loss, providing a tax deduction in the year of disposal. If equipment is disposed at or after full depreciation, there is no remaining book value to write off, but any resale proceeds are assessable income.

The net financial outcome depends on the balance between the write-off benefit (for early disposal), the resale value (which declines with age), and the cost of continuing to operate older equipment (higher maintenance, reduced productivity, increased security risk).

For organisations optimising their financial position, the ideal disposal timing minimises total cost across all of these factors, which often does not coincide neatly with the depreciation schedule endpoint.

Refresh Cycles vs Depreciation Schedules

Many organisations align their technology refresh cycles with their depreciation schedules, but this alignment is not always optimal. Consider running the numbers on different refresh cycle lengths, including the resale value at each potential disposal point. For laptops, a comparison might look like this.

At three years, the remaining book value is $500 (under straight-line depreciation of a $2,000 laptop), but the resale value might be $400-600. The write-off of remaining book value provides a tax benefit, and you capture strong resale value.

At four years, the book value is zero, and the resale value has dropped to perhaps $150-300. There is no remaining depreciation to write off, and you have spent an extra year paying for maintenance on older equipment.

At five years, the book value has been zero for a year, resale value is minimal ($50-100 at best), and you have incurred two additional years of increased maintenance and reduced productivity. The differences compound across large fleets.

Asset Register Integration

Your asset register should track both the depreciation status and the planned disposal date for each device. These may be different dates, and tracking both allows you to plan disposals that optimise the financial outcome while meeting operational needs.

Flagging assets that are approaching the end of their depreciation schedule prompts timely evaluation of whether to continue using, redeploy internally, or dispose of each device. This proactive approach is better than waiting until equipment fails or becomes a nuisance.

Incorporating disposal planning into your broader IT asset lifecycle management ensures that depreciation schedules inform but do not dictate disposal timing.

Communicating with Finance

IT and finance teams sometimes have different perspectives on disposal timing. Finance may prefer to run equipment until it is fully depreciated to avoid write-offs. IT may prefer earlier refresh to maintain performance and reduce support burden. Both perspectives are valid, and the optimal decision lies in the data.

Present the complete financial picture: the write-off cost of early disposal, the resale value captured, the avoided maintenance and support costs, the productivity impact, and the security risk reduction. When all factors are considered together, the case for disposal timing based on total value rather than depreciation schedule often makes itself.